Markets have a pattern. A great story emerges. Capital floods in. Valuations stretch. Extrapolation takes over and the story becomes the entire market.

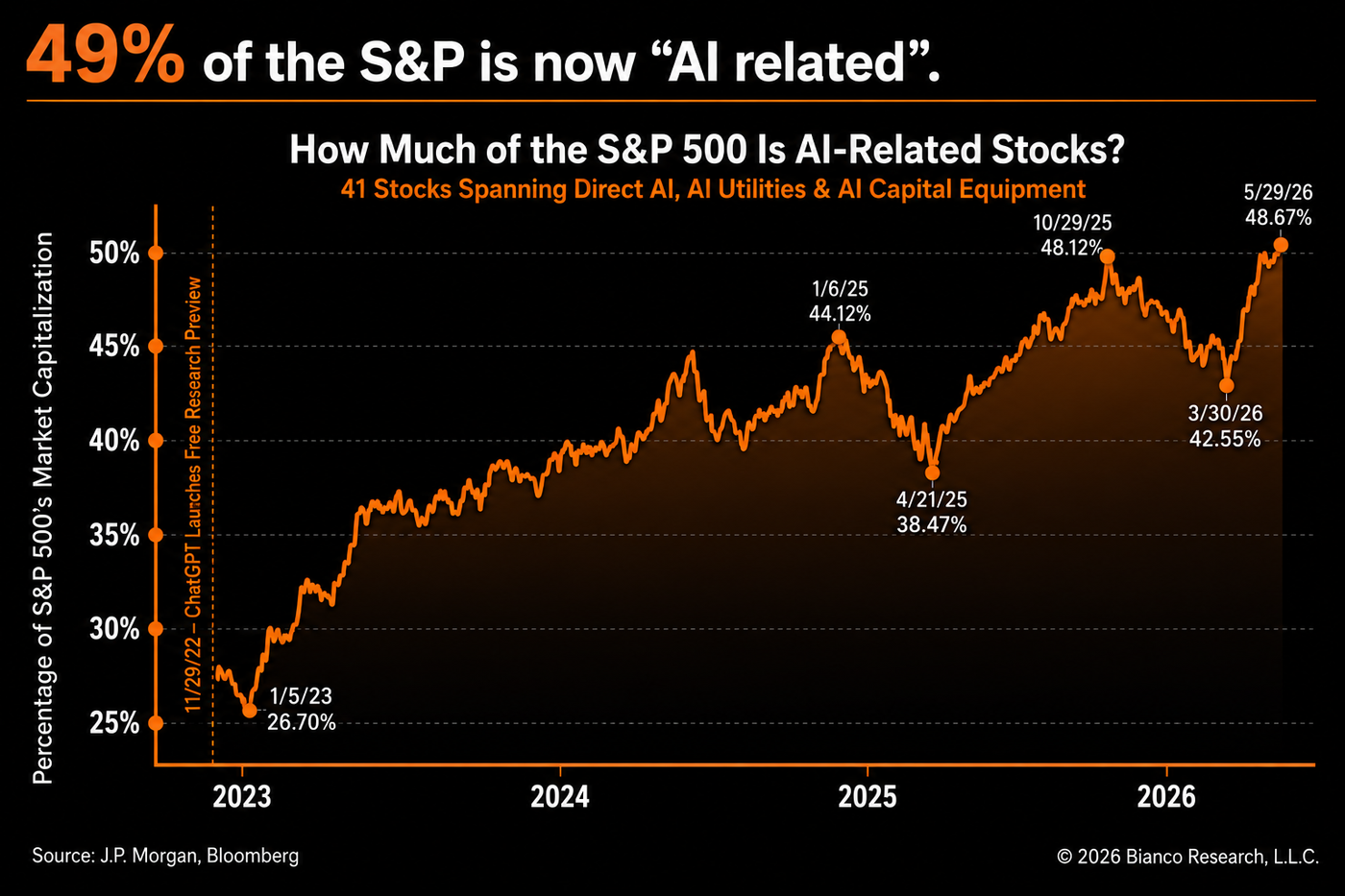

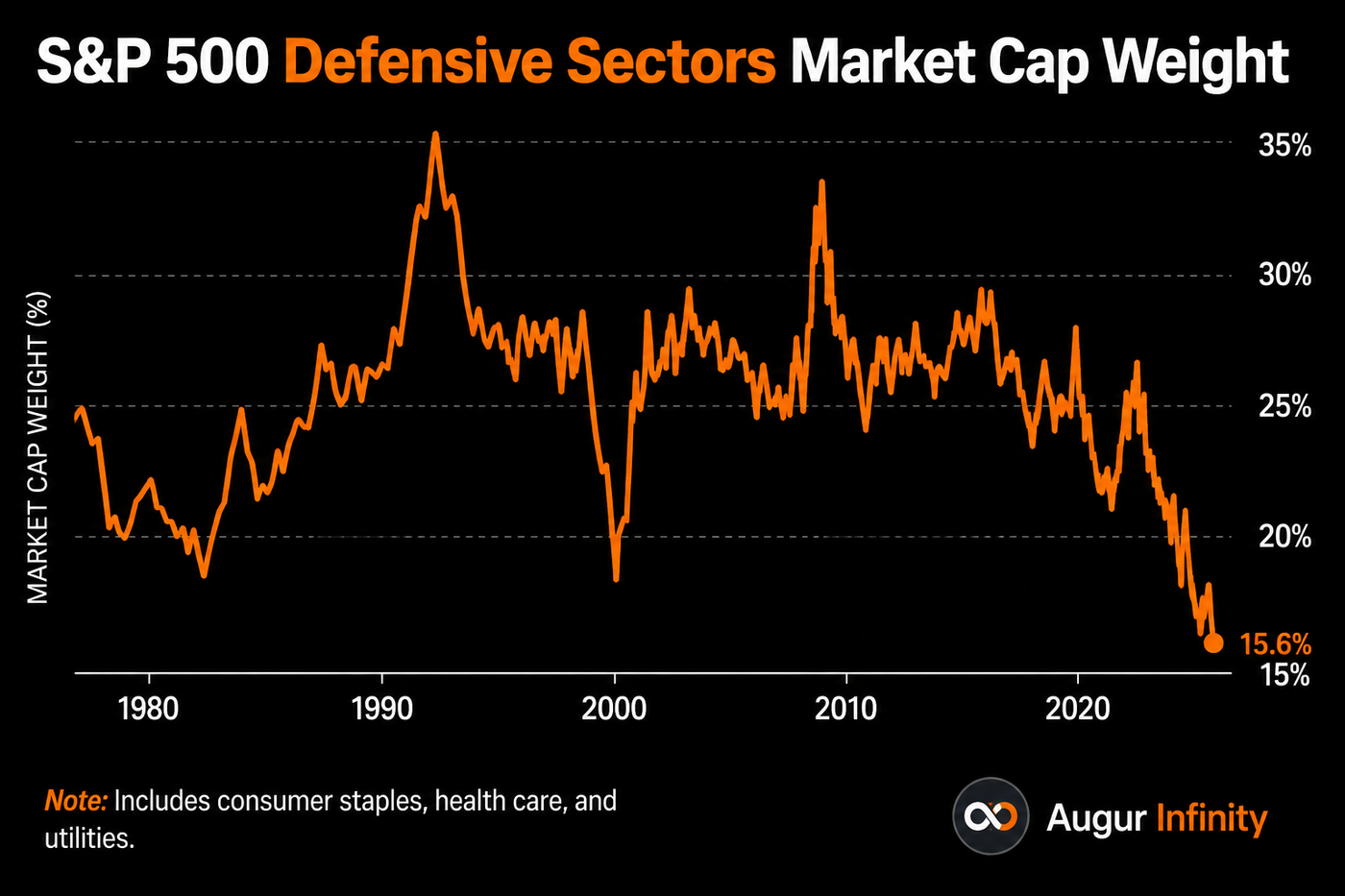

That’s where we are. The companies powering the AI revolution now represent roughly half the S&P 500 and a comparable share of US economic output. Concentration, momentum, and speculative sentiment have reached levels historically associated with major market peaks. Defensive assets — government bonds and consumer staples — have suffered historic drawdowns as capital abandoned anything that wasn’t AI.

We’ve seen this movie. Nifty Fifty. Dot-com. The storyline changes. The math doesn’t.

Bubbles don’t end on schedule. The final phase often delivers the strongest gains — peak FOMO, right before the turn. That makes timing the exit nearly impossible. What it doesn’t make impossible is positioning now for where capital goes next.

History’s answer is consistent: after extreme concentration, markets broaden. The assets left behind during the mania become the leaders of the recovery.

Today’s most left-behind asset class? Emerging markets. Or so it appears.

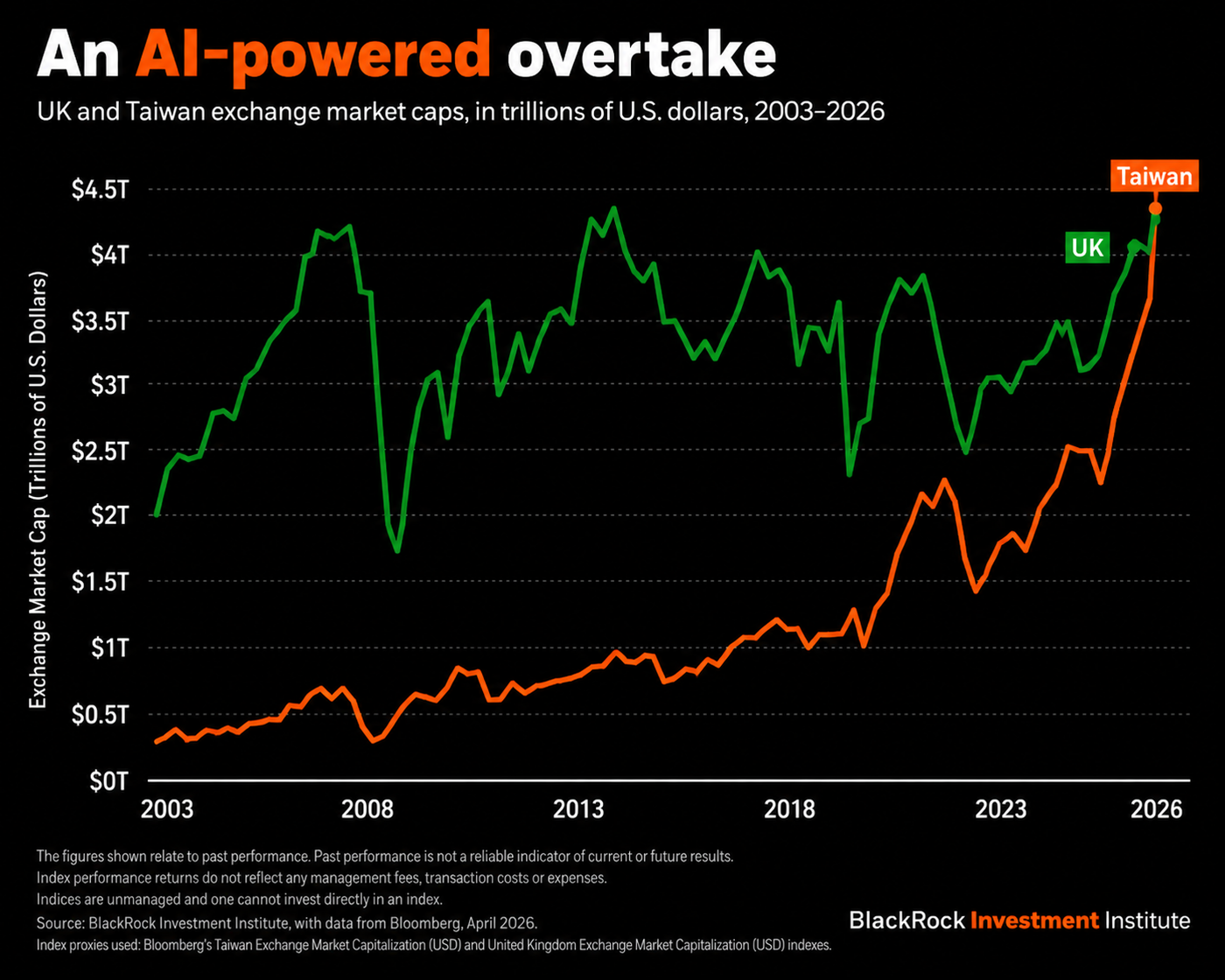

The AI boom hasn’t stayed in America. Taiwan and South Korea; two of the world’s most technology-intensive economies now dominate emerging market indices in ways that would have been unimaginable a decade ago. Taiwan’s weighting in the MSCI EM Index now equals China’s. South Korea’s KOSPI has nearly tripled in the past year.

The consequence is one most investors haven’t priced in: the average emerging market portfolio now carries 20–50% exposure to AI-related companies. That’s not diversification from the US market’s concentration in AI — that’s doubling down on it.

Flextion remains convinced that non-US equities, including emerging markets broadly, are positioned to outperform over the next decade. But tactically, the more compelling risk-reward sits with funds that have limited exposure to semiconductors, servers, and AI infrastructure — the crowded trade hiding inside the EM label.

We screen for these opportunities across three categories: small cap, defensive, and broad EM strategies with lower AI overlap. The funds below score highest on Flextion’s AI rankings and are best positioned to lead when the current cycle turns.

History’s answer is consistent: after extreme concentration, markets broaden. The assets left behind during the mania become the leaders of the recovery.